I am excited to share the latest paper with Prof. Alexander Lipton.

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4035813

We find the semi-analytical solution to one of the unsolved problems in Quantitative Finance, which is to compute survival probabilities and barrier option values for two-dimensional correlated dynamics of stock returns and stochastic volatility of returns.

An analytical solution to such a problem does not appear feasible because the valuation equation is asymmetric in the log-price variable when the correlation between returns and the volatility of returns is non-zero. In the case of zero correlation, an analytic closed-form solution is achievable involving a numerical integration in the Fourier space.

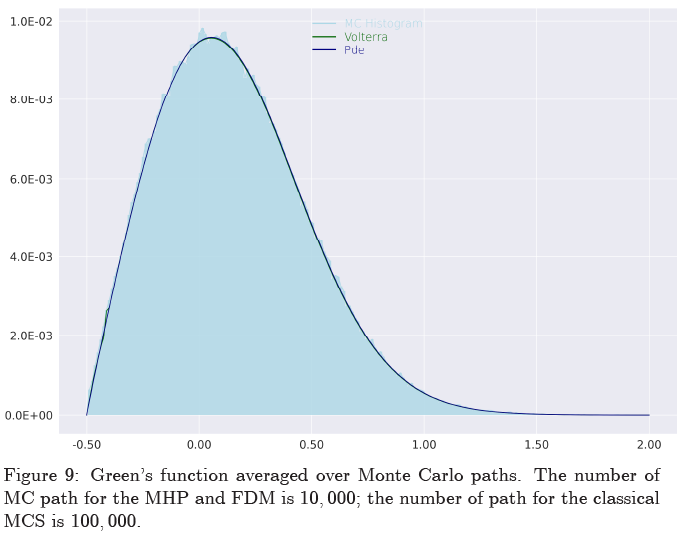

In this article, we combine one-dimensional Monte Carlo simulations and the semi-analytical one-dimensional heat potential method (MHP) to design an efficient technique for pricing barrier options on assets with correlated stochastic volatility. Our approach to barrier options valuation utilizes two loops. First, we run the outer loop by generating volatility paths via the Monte Carlo method. Second, we condition the price dynamics on a given volatility path and apply the method of heat potentials to solve the conditional problem in closed-form in the inner loop. Next, we illustrate the accuracy and efficacy of our semi-analytical approach by comparing it with the two-dimensional Monte Carlo simulation and a hybrid method, which combines the finite-difference technique for the inner loop and the Monte Carlo simulation for the outer loop. Finally, we apply our method to compute state probabilities (Green function), survival probabilities, and the value of call options with barriers.

As a byproduct of our analysis, we generalize Willard’s (1997) conditioning formula for valuation of path-independent options to path-dependent options. Additionally, we derive a novel expression for the joint probability density for the value of drifted Brownian motion and its running minimum or maximum in the case of time-dependent drift.

Our approach provides better accuracy and is orders of magnitude faster than the existing methods. The methodology is general and can equally efficiently manage all known stochastic volatility models. Besides, relatively simple extensions (will be described elsewhere) can also handle rough volatility models. With minimal changes, one can use the method to price popular double-no-touch options and other similar instruments.