Year 2018 was eye-opener for investors in alternative risk-premia products. A lot of these products have been sold as market-neutral but they did not live up to expectations… I think, the reason is simple: most of ARP products have been driven by marketing with nice looking back-tested results obtained by over-fitted models. I made a presentation on this topic back in early November 2018. Yet, traditional alternatives had a bad year too.

We published an article in the Hedge Fund Journal to explain the difference between traditional trend-following CTAs and Alternative Risk Premia. Here I will post the introduction and the key insight from our model to define the risk-premia alpha.

Introduction

The turbulence of 2018 made it a difficult year for most systematic investment products. To the surprise of several investors, many of these quant products had been sold as market neutral. In particular, the new breed of alternative risk-premia (ARP) products – that had flooded the market a few years prior to 2018 – performed exceptionally badly. For example, the composite HFR Bank Systematic Risk-premia Multi-Asset Index lost -18%, in comparison with a loss of -4% on the S&P 500 total return index. However, traditional alternative asset classes also underperformed, with the flagship HFRX Global Hedge Fund Index losing -7% and the SG Trend Index losing -8%.

In the face of such losses, both investors and managers are asking how and why so many quant strategies underperformed? Still more importantly, what are the implications for the diversification of traditional equity-bond portfolios and alternative investments? In particular, since trend-following CTAs belong to a handful of tried-and-tested diversifiers, why did trend-followers not diversify in 2018?

To address such questions, we first intend to look at how trend-following programs are expected to perform when crises last for extended periods of at least two months, because trend-followers need to adjust to profit from sustained crises in equity markets. Second, we shall focus on the way in which the risk profile of ARP products, hedge funds, and trend-following CTAs can change in bear and bull market regimes because of their potential exposures to tail-risk. We analyse the risk-premia alpha in these products by taking into account regime-conditional risk.

For this analysis, we are proposing a new quantitative model to explain the risk of investment strategies by accounting for extreme market conditions and for their exposure to tail risk, such as selling volatility and credit protection. We apply this model to the cross-sectional risk attribution of about 200 composite indices of hedge funds and ARP products. We show that there is a strong linear relationship between risk-premia alpha and the tail risk of systematic ARP strategies. We can demonstrate that our model explains nearly 90% of the risk-premia for volatility strategies and about 35% of the risk-premia for hedge fund and ARP products. In this way, most ARP and hedge fund type products can be seen as risk-seeking strategies. Importantly, our model predicts that ARP products offer smaller risk-premia compensation compared to hedge funds.

We are able to illustrate that, interestingly, trend-following CTAs are exceptions since they belong to defensive strategies with negative market betas in bear regimes, yet risk-premia alphas for CTAs are insignificant. CTAs cannot be seen either as ARP products with positive risk-premia alpha from exposures to tail risk, or as defensive products with negative risk-premia designed to reduce tail risk, such as long volatility strategies. Instead, trend-following CTAs should be viewed as an actively managed defensive strategy with the goal to deliver protective negative market betas in strongly downside markets along with risk-seeking positive market betas in strongly upside markets. Overall, after adjusting for the downside and upside betas, the risk-premia alpha of CTAs is insignificant. Yet, because of the negative protective betas in bear markets, trend-followers well deserve their place as diversifiers in alternative portfolios to improve risk-adjusted performance and capture risk-premia alpha on a portfolio level, as we will show in the last section.

Finally, since our risk-attribution model assumes conditional equity betas in specific market regimes, we are able to illustrate the misunderstanding behind strategies claiming to be “zero-correlated” and “market-neutral”. Given a specific market regime, most typically in the bear regime, many risk-premia strategies tend to produce a strong exposure to equity markets because of their hidden tail exposures. For example, a strategy selling delta-hedged put options would have a small market beta during normal regime; yet the strategy would exhibit a significant market beta during crisis periods because of its negative gamma and vega exposures. When we analyse systematic strategies unconditional to market regimes, the performance may appear to be smooth and uncorrelated because of the aggregation across different regimes.

We will conclude the introductory section and our article by answering the above questions in the following way. Firstly, ARP strategies are expected to perform well during normal regimes. However, since the excess performance of these strategies is derived from a hidden tail risk, these strategies are expected to underperform during turbulent markets, as in 2018. To earn risk-adjusted alpha from these products, investors need to look at long time horizons that include both bull and bear markets. Second, while the performance of trend-following CTAs is not derived from risk-premia alpha as compensation for hidden tail risks, the performance of trend-followers is conditional on trends lasting for sustained periods. Since trends reversed rapidly multiple times during 2018, trend-followers underperformed. As a result, in what proved to be an extraordinary year, both ARP products and trend-followers underperformed, but for different reasons.

Going forward, investors and allocators need to understand how different strategies are expected to perform during bear and normal markets and how to diversify their portfolios accordingly. Our results provide a valuable aid in quantifying the hidden tail behaviour of systematic strategies as well as suggesting an approach for the risk attribution and diversification of alternative portfolios.

Risk-premia Alpha

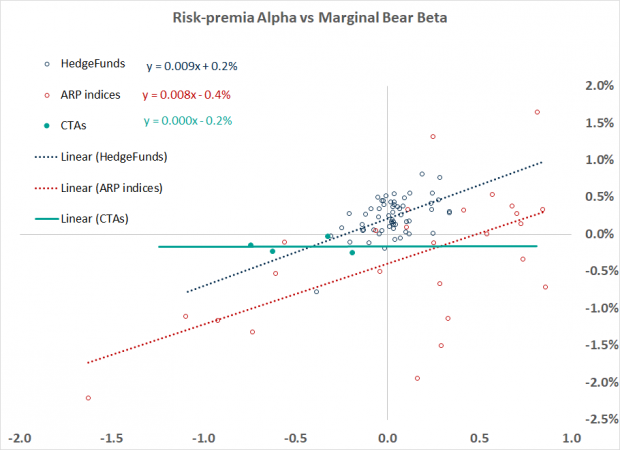

Risk-premia alpha measures the excess return on a strategy after adjusting for conditional beta exposures. According to the regime conditional CAPM, a strategy should produce higher risk-premia alpha if it assumes higher equity risk in a bear market measured by marginal bear market betas.

The figure in the top illustrates different risk profiles of hedge fund and ARP products. We apply the regime conditional model to a large universe of indices grouped into three categories:

- Hedge fund indices from major index providers including HFR, SG, BarclayHedge, Eurekahedge with the total of 73 composite hedge fund indices excluding CTA indices;

- 7 CTA indices from the above providers; and

- ARP indices using HFR Bank Systematic Risk-premia Indices with a total of 38 indices.

According to our model we see a clrear differentiation among risk-seeking strategies, defensive strategies and trend-following CTAs.

Risk-seeking strategies: the marginal bear beta is positive (increased risk in bear regime) compensated by positive risk-premia alpha. Most hedge fund and ARP products are risk-seeking strategies with tail risk. We observe almost a linear relationship between risk-premia alpha and marginal bear betas for the cross-section of hedge funds and ARP indices. ARP products deliver less risk-premia alpha for the same level of tail risk compared to hedge funds.

Defensive strategies: the marginal bear beta is negative (reduced risk in bear regime) compensated by negative risk-premia alpha. Defensive strategies diversify equity risk in bear regimes but deliver negative risk-premia alpha.

Trend-following CTAs: produce negative marginal bear market betas and hence strongly diversify equity risk in bear market regimes. Because their risk-premia alpha is flat, trend-followers can be considered as an anomaly, or as a differentiation from ARP and traditional hedge fund products.

One thought on “Trend-Following CTAs vs Alternative Risk-Premia (ARP) products: crisis beta vs risk-premia alpha”

Pingback: Alternative Links: Stocks Get Lift From Earnings as Traders Await Feds - RCM Alternatives