Exchange traded products with the short exposure to the implied volatility of the S&P 500 index have been proliferating prior to “Volatility Black Monday” on the 5th of February 2018. To investigate the crash of short volatility products, I will analyse the intraday risk of these products to steep intraday declines in the S&P 500 index. As a result, I will demonstrate that these products have been poorly designed from the beginning having too strong sensitivity to a margin call on a short notice. In fact, I estimate that the empirical probability of such a margin call has been high. To understand the performance of product with the short exposure to the VIX, I will make an interesting connection between the short volatility strategy and leveraged strategies in the S&P 500 index and investment grade bonds. Finally, I will discuss some ways to reduce the drawdown risk of short volatility products.

Key takeaways

- Exchange traded products (ETPs) for investing in volatility may not be appropriate for retail investors because, to deliver the lasting performance in the long-term, these products need risk controls and dynamic rebalancing to avoid steep drawdowns and to optimise the carry costs from the VIX futures curve.

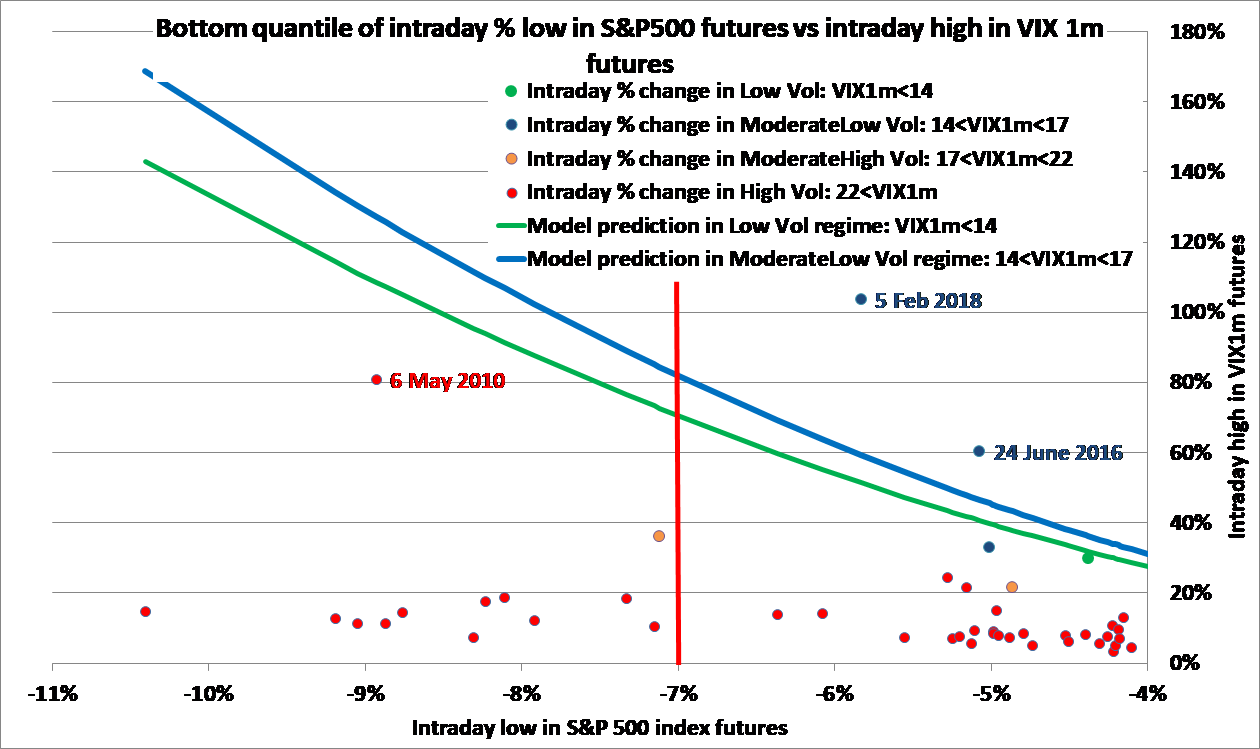

- The convexity of VIX changes and the sensitivity of changes in the VIX futures to changes in the S&P 500 index is extremely high in regimes with low and moderate levels of the implied volatility. As a result, a margin call on short volatility ETPs is more likely to occur in periods with low to medium volatility rather than in periods with high volatility.

- Without proper risk-control on the notional exposure, ETPs with the short VIX exposure are too sensitive to the intraday margin calls on a very short notice. Empirically, in the regimes with medium volatility, an intraday decline of 7% in the S&P 500 index is expected lead to 80-100% spike in the VIX futures and, as a result, to margin calls for short volatility ETPs.

- Short volatility ETNs provide with a leveraged beta exposure to the performance of the S&P 500 index, there is no alpha in these strategies. This leveraged exposure can be replicated using either S&P 500 index with leverage of 4.2 to 1 or with investment grade bonds with leverage of 9.6 to 1. All these strategies perform similarly well in a bull market accompanied by a small realized volatility and significant roll yields, yet these leveraged strategies are subject to a margin call on daily basis.